What is an Omnichannel Payment?

The term “Omnichannel” has become a buzzword in the payments industry, and it is just the beginning. Let’s go deeper and see what is behind the curtains!

Omni comes from Latin, and it simply means “all.” What we refer to as channels are, in fact, different venues of accepting credit card payments.

There are two kinds of credit card acceptance:

- Card-Present: This is when a customer hand you a credit/debit card, and you run it through a “terminal.”

- Card-Not-Present: You process a transaction without access to the physical card, and you have only access to its number, expiration date, and few other pieces of information.

Consider the Following scenarios in accepting a credit card payment:

- eCommerce and online shopping: You, the merchant, have no access to your customer’s credit card, and the customer fills out a form on your website to provide you with card information for processing. This scenario is a card-not-present one.

- Accepting the card over the phone: The cardholder is not present, and he provides you with his card information, either by speaking to a representative or in response to an automated system.

- When you are accepting payments on your cell phone, a card reader is attached to your phone, and you can either swipe the card or dip it (in case of chip cards). This transaction is an example of card-present.

One more thing to remember is that in some cases, even when the customer is in front of you and gives you a card to charge, you may end up keying the card number into a credit card machine or software to process the card. In this case, you have a card-not-present. Unless a card is swiped, dipped, or tapped to a processing device, otherwise, the transaction is going to be considered card-not-present.

A payment channel is a venue or outlet through which customers make a purchase, pay bills, or pay for services.

When you run an eCommerce website, your website is a channel. The credit card machine on your countertop is used in your in-store channel to accept payments.

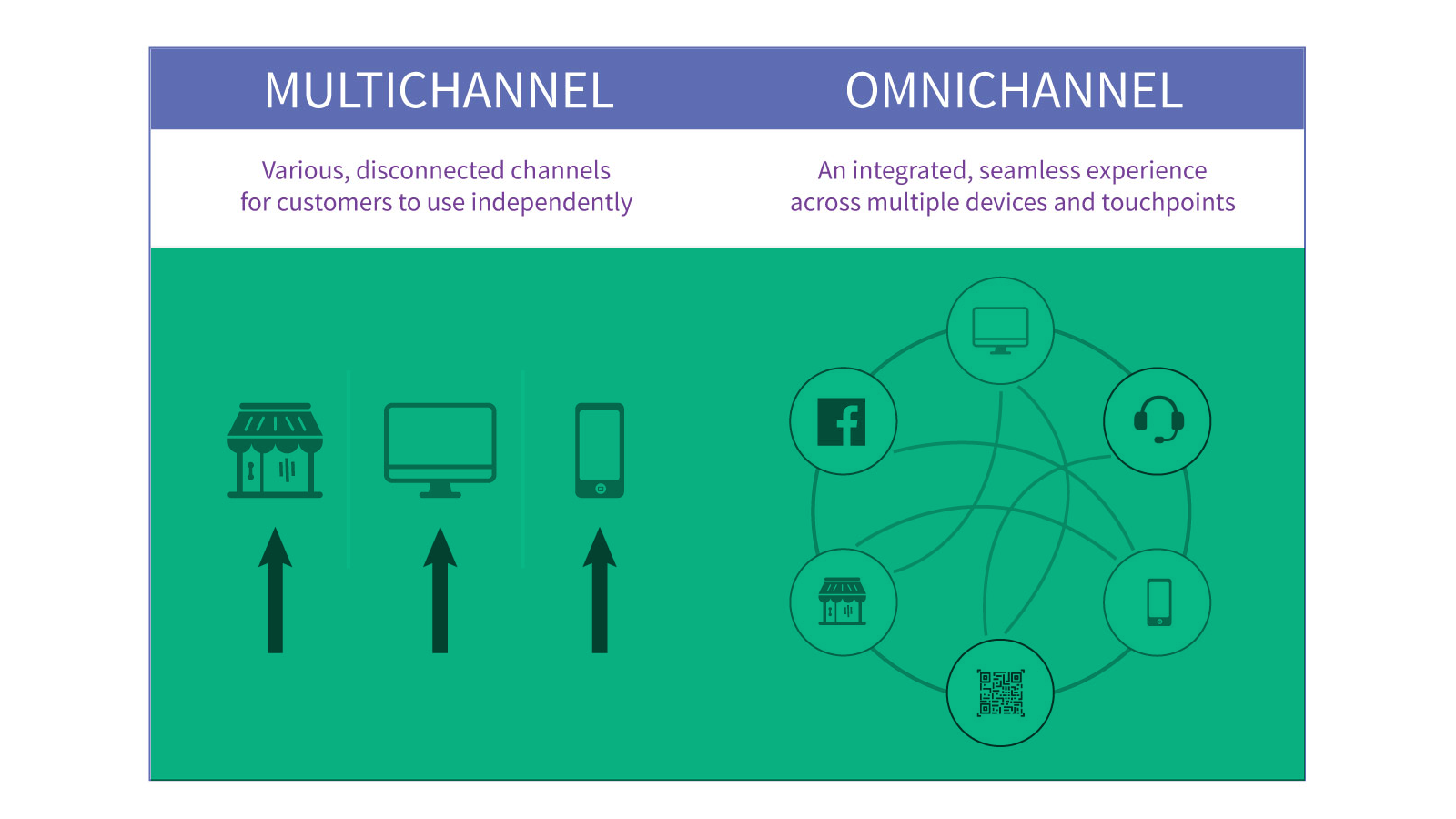

Omnichannel vs. Multichannel

When you have multiple sales channels, but your channels are not interacting with each other, you only have a multichannel. In a true Omnichannel, your channels are interconnected, and you can follow transactions from one channel and process them on your other channels.

For example, if you have a shoe store, and you also offer the same shoes on your website, you need to accept payments from both channels.

If a customer goes to your website and orders a pair of shoes:

- A payment received on the website, and you should have records of it.

- A card-not-present transaction took place on your website.

- After the customer receives the shoes, he finds out that they are too small. The customer comes to your store (maybe because you are in the same city as the customer) or calls you on the phone to request an exchange or refund.

- You want to be able to ask for the customer’s card and make a refund by swiping or keying the card.

All payments records, regardless of their point of origin, AKA Channel, should be available for you to perform a transaction such as above.

This scenario presents the need for “Omnichannel” payment processing.

By now, you should see the critical role payment processors can play in providing the Omnichannel payment solutions that would process transactions from many channels (mobile devices, websites, in-store) through a single processing platform.

Providing a seamless and effortless consumer interaction experience has become an inevitability for merchants in a hyper-competitive market environment. Nevertheless, too often, there is a wide gap between customer expectations and merchant abilities, with merchants facing many problems.

Having said all these, I should add that many businesses do not need an omnichannel solution.

If you receive payments from multiple channels (online, in person, over the phone, mobile apps, etc.) then your options are limited to the following:

1- work with more than one processor and obtain more than one merchant accounts separately for each channel

2- Work with one processor that can offer an all-in-one payment processing solution or Omnichannel.

After you identified your payment channels and methods, you will need to find merchant service providers that can process cards in your channels and ways.

Working with one processor is not easy, let alone dealing with multiple processors! No way. You will be better off with having multiple accounts with one processor and deal with only one customer service. You could use one account for your card-present transactions and another one for your card-not-present. However, it is imperative to work with a process that offers Omnichannel solutions so that you can extend the kind of service; every customer expects from a retailer.

I hope that I have been able to make it clear that Omnichannel is more than just a buzzword; it is becoming a necessity for any business to provide convenient and secure payment methods to their customers.