The Elephant in the room

What I have discussed in this article is a genuine case of the Elephant in the room. Unless you are very new in the payment processing industry (your first few weeks), otherwise you know that this industry has a big problem that while everybody is aware of it, but nobody is ready or willing to step forward and discuss it.

Businesses do not trust credit card processing companies.

FTC Files First Complaint Concerning Credit Card Merchant Account Sales and Billing Practices

Elavon Gets Sued Over Excessive PCI Compliance Fees

Wells Fargo Merchant Services Lawsuit

Retailer Wins Lawsuit Against Its Merchant Processor

Payment Card Interchange Fee Settlement

Visa, Mastercard reach $6.2 billion settlement over card-swipe fees

Credit Card Provider Sued for ‘Deceptive’ Tactics

Worldpay US Credit Card Processing Hidden Fees and Charges Class Action

It is an uncomfortable subject to discuss the problem of lack of transparency, honesty, and in some cases, a total lack of morale in any industry.

With its natural and direct connections with businesses, the payment processing industry has gained itself a bad reputation.

I interviewed several professionals in the industry and sought their opinion. Without exception, everybody acknowledges that many credit card processing companies will exploit their merchants and betray their trust.

I am opposed to the notion that:

“You cannot trust credit card processing companies.”

It is unfair to paint with a broad brush, although in many cases, you could question the trustworthiness of a processor.

In this article, I will discuss trust and transparency when it comes to credit card processing companies.

In essence, a processor is like a partner of the business who collects his percentage, regardless of profit or loss. Business-Processor relationship, like any other business relationship, requires honesty, transparency, and trust to last.

I have worked for the credit card processing companies that are among the best, with the highest degree of integrity and transparency, in the industry. I have also worked with many of them as a developer. There are great companies in this industry who treat their merchants with integrity and transparency.

Undeniably, some processors take advantage of their merchants, and deceive them.

Unfortunately, the credit card processing industry has a bad reputation when it comes to honesty. I, personally, believe that the mistrust has its roots in distrust of the Banking system among the general public.

In essence, a processor is like a partner of the business who collects his percentage, regardless of profit or loss. Business-Processor relationship, like any other business relationship, requires honesty, transparency, and trust to last.

When a merchant decides to use a different processor, it’s the processor’s loss and not the business.

Let’s see when this all started and why it has continued to be an issue.

The Devil is in the Details

Merchant Statements

For a cash-only business that does not accept credit card payments, there are no costs in receiving payments. Still, the cost of doing business is higher because they lose a significant number of customers who use credit cards for payments. As the global banking systems and economies pursue cashless societies, the cash-only business model becomes obsolete, irrelevant, and eventually impossible.

Accepting credit card payments by merchants is not a matter of choice any longer. It’s a requirement if they don’t want to lose nearly 80% of their sales. On the other hand, people tend to spend more when they pay with a credit card.

Whether merchants know it or not, when they receive deposits, they receive an unsecured line of credit from the ISO or MSP. Like all other loans, there are fees to service the loan, and the merchant is responsible for the costs.

For the most part, fees and costs of processing are straight forward. Interchange rates announced twice a year by the card networks, and in theory, everything else should follow.

Some credit card processing companies figured out that the fastest and easiest way to make more money is to increase rates and fees. They can’t sign business fast enough to equal what they could make the next month because of an added fee or rate increase.

It is essential to know that any bank or ISO that offers merchant services assumes the risk of financial losses. So, the vetting of a merchant before providing a merchant account is essential for the ISO. Every merchant service provider wants to minimize their exposure to losses.

The moment a merchant decides to use a specific processor’s service, he has trusted them. If the sales agent is an old friend or a relative or referred by another friend, the degree of trust is even higher.

So, why is there so much outcry over credit card processing fees?

Facts:

- Many merchants never review their monthly credit card processing Statements that they receive from their processor.

- Many merchants don’t know how the credit card processing models work and what’s best for them.

- Many merchants don’t know how much they pay for credit card processing or their rates.

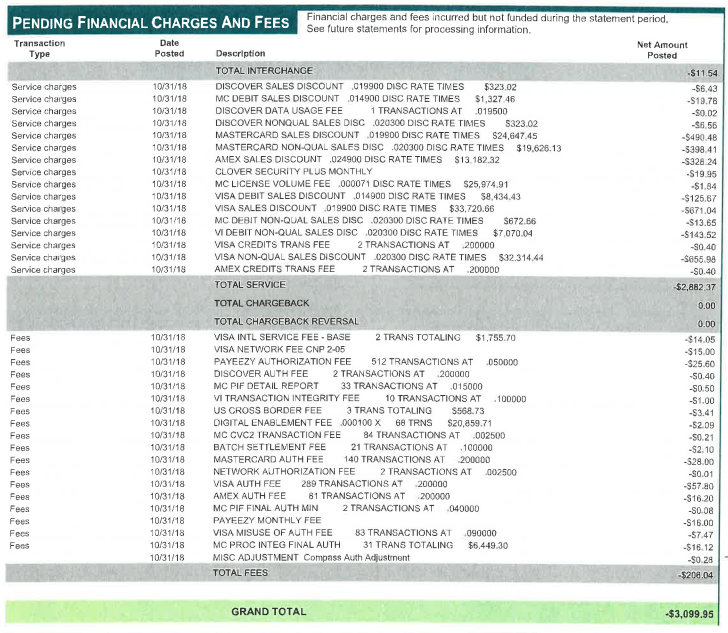

- Credit card statements are complicated, vague, very long, and nearly always hard to decipher.

- Statements from different processors are different in format, amount of information they present, and complexity.

- There is little or no education for merchants about the payment processing and its details.

- The rules change often, and the only place you can find them is in the fine prints of Statements.

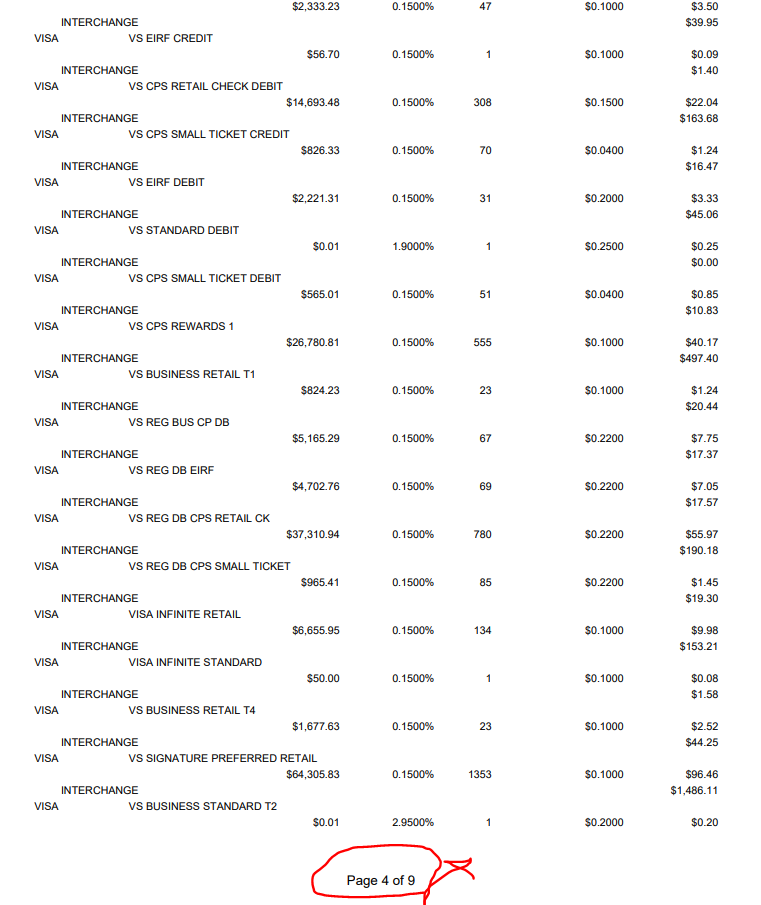

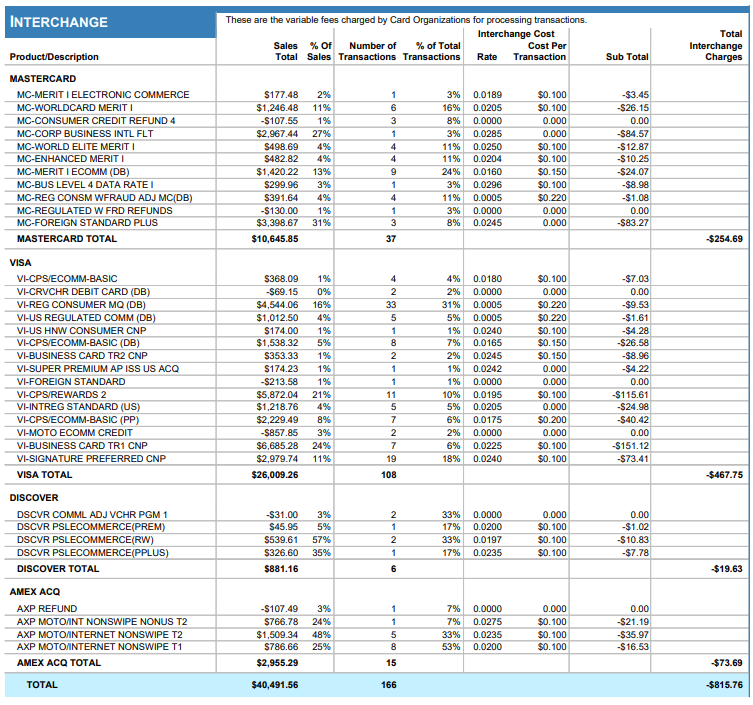

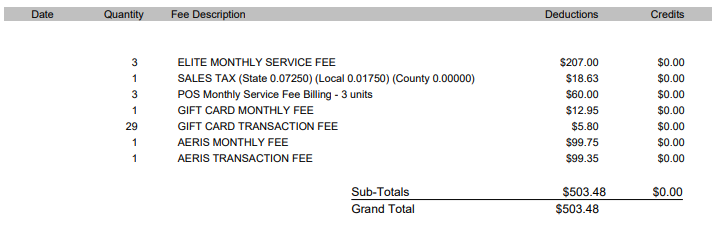

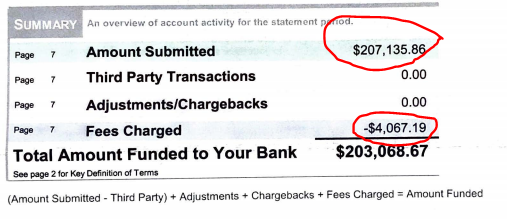

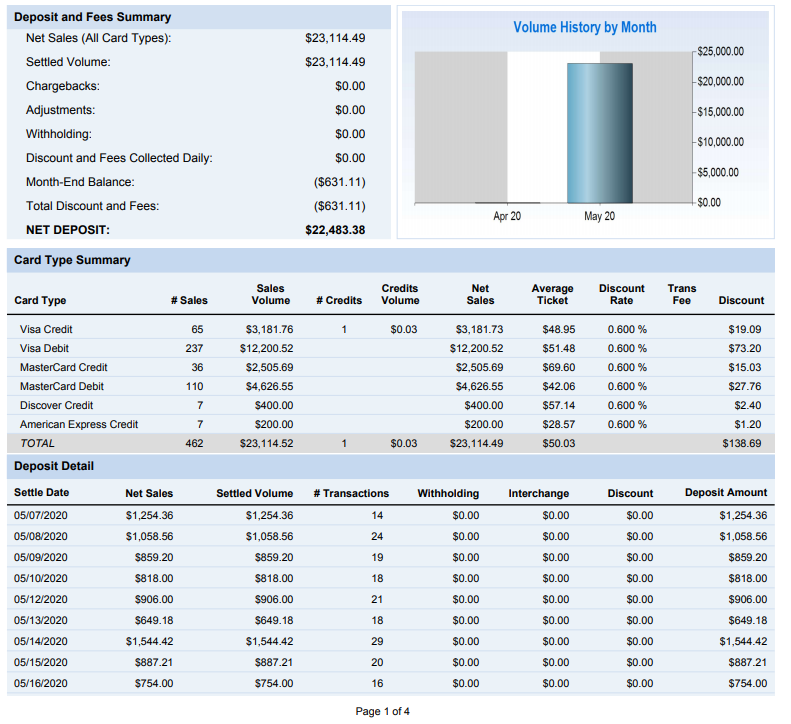

The main parts on any Statement present the details of each card processed, type of card (commercial, personal, or otherwise.), transaction tier, and more.

You will also find a list of applicable fees on each Statement.

There is a long list of additional fees that a processor could add to the overall processing cost.

The following are some of the common fees:

- Statement fees

- Monthly Service fee

- Monthly Minimum Fee (if applicable)

- Monthly Gateway fee (if applicable)

- Transaction fees

- Batch fee

- AVS fee (applies to card-not-present in sales)

- PCI Compliance Program

- Chargeback Fee (if applicable)

- Annual Fee (if applicable)

- Device lease fees

It is not unusual to find fees that are not common on other Statements.

According to the rules established by Visa and MasterCard, ISOs could raise the prices on their merchants anytime they want, so long as they inform the merchant in advance.

Guess where the information regarding price hikes is? You guessed it right, buried in the Statement.

ISOs could also change, add or waive some of their fees. Fee details are also on the Statement fine prints.

Effective Rates

Let us look at a simple method that could give the merchants a clue about their processing rates:

Every business gets visited by sales agents from different processing companies a few times a week.

The first thing any sales agent would request is the copies of recent statements from the merchant.

Unfortunately, when specific merchants are “stuck” in a situation where they cannot change their processor easily, the ISO takes advantage of them.

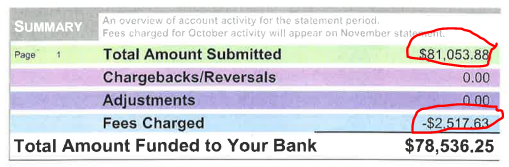

The process begins once the prospect ISO receives the statements. The most basic information from the Statement is the “effective rate.”

The effective rate is the total amount of charges as fees by the total processing volume.

For example, if the total volume is $100,000 and the total fees are $3000, the effective rate is 3.0%.

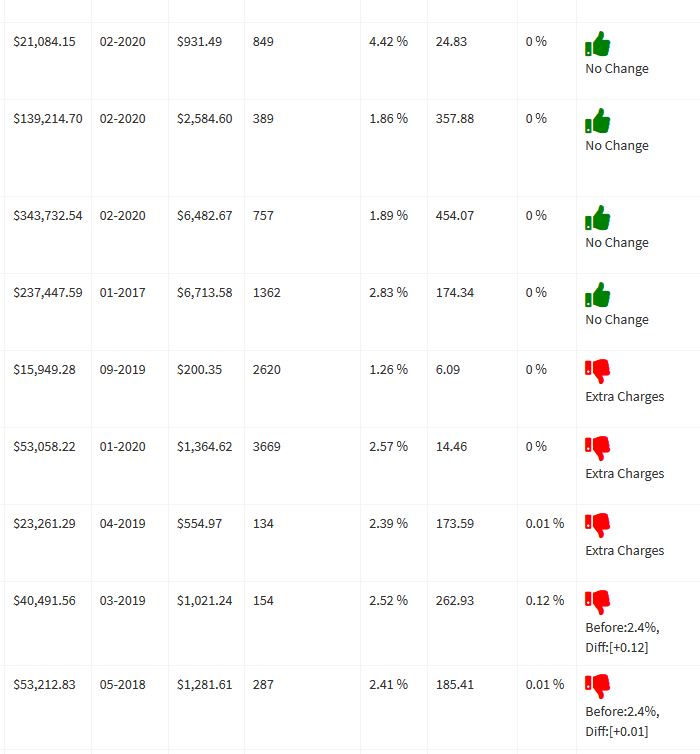

The effective rate includes all fees and expenses. But if you try to calculate the effective rate on three different statements for the same merchant, you likely come up with three different numbers!

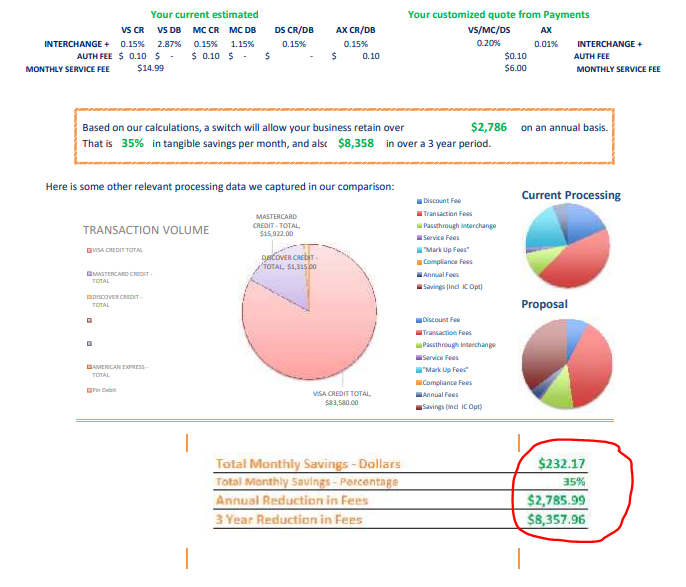

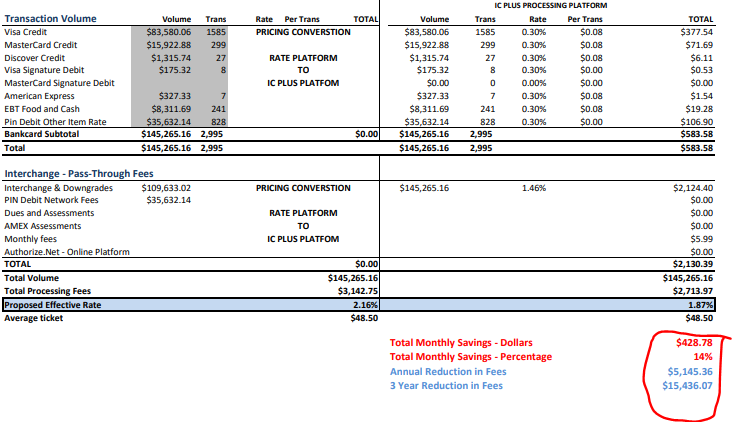

Look at the following three proposals from three different processors, for the same merchant:

The first and second proposals have a slight difference in proposed savings, but the third proposal claims to save the merchant more than $200 compared to the first and second proposals!

As a metric, the effective rate is not reliable, but we can rely on it just as an indicator.

Once there is a higher ER, the merchant needs to review the entire Statement to determine what has changed and how the changes affected the overall processing.

Statements are not easy to read. So, you can see that we are back to square one!

Honesty and Transparency

Credit Card Processing industry is extraordinarily competitive. Merchants switch their processor, on average, every two years.

I don’t believe that the question of honesty about an ISO is black or white. It’s complicated.

In other words, ISOs lose merchants daily and need to recruit new merchants every day.

Sales agents make their money when they sign up new merchants, and as long as a merchant stays with the same processor, the sales representative will have a residual income from the account.

Part of the problem comes from the fact that recruiting new merchants is not easy in a competitive market. Some Sales agents make promises that won’t be able to keep, that could be knowingly or unknowingly.

To solve the issues initiated by the sales agents, some ISOs hire their sales team as W2 employees. So, benefits from being an employee create a more relaxed environment for the sales team. Nevertheless, the pressure to make cold calls, schedule appointments sign up new accounts is still high.

I know that many sales agents work hard to keep their merchants well informed. They visit the businesses on a weekly or at least monthly basis and talk to them.

I know many ISO that although they have W2 employees, they require a, sometimes unreasonable, very high quota for each representative, or they lose their job.

So, my point is that the sheer amount of pressure on the sales teams could lead to behaviors that are less than honest.

In many cases, when the honesty of an ISO is at the question, we have to look at the company’s overall culture.

When ISOs add Point of Sale to the mix, the longevity of an account is much higher and, therefore, the opportunities to raise the fees on the merchant, which could very well be a captive audience, because of the POS.

I have seen rates as high 5% on accounts where a specific processor has an exclusive deal with a software product.

Although it’s not fair to call every sales agent or ISO, dishonest, you can see that on some occasion, it’s a question of morality and decency.

I have seen a lot more great individual sales agents with integrity and transparency, then processing companies.

Unfortunately, when specific merchants are “stuck” in a situation where they cannot change their processor easily, the ISO takes advantage of them.

Credit card processing companies figured out that the fastest and easiest way to make more money is to increase rates and fees. They can’t sign business fast enough to equal what they could make the next month because of an added fee or rate increase.

Once merchants find out about the new rates or fees, the first reaction is most likely not a pleasant one.

They look for another processor. Switching to a new processor is not always easy. Many things must be changed, or updated and it takes a while for the merchant to “get used to” it, especially if there is a POS system involved. Thanks to semi-integrated solutions, such as Pax, the POS PIN pads could be re-programmed to use a new processor.

Pass the bucket

In recent years, many ISOs push models such as Surcharging and Cash Discount, to offset the cost of credit card processing for the merchants, by passing along the cost to customers.

Neither of these models is going to build a better relationship between a merchant and its ISO.

On the one hand, Vias and Mastercard push back against Surcharge and Cash Discount, and on the other hand, consumers, object to the additional costs.

How would you react if, for a $100 check, you have to pay 4% for credit card processing, 5% COVID fee, and a sales tax on top of that?

We cannot solve the problem of honesty, integrity, and transparency with burdening the customers and passing the bucket. In most cases, when a merchant uses Surcharge or Cash Discount, the ISO charges a higher fee for processing.

We need a method for merchants to keep an eye on their Statements, month after month, and be able to identify the changes.

Not all changes are illegitimate and unlawful. But merchants need to know about all changes and receive good explanations form their ISOs.

Solutions

Education

Merchants and business owners need to have access to information and learning material to educate them about the payment industry in general and understanding of their monthly statements in particular.

You might say this information is available on the web, and I say yes. But except for a tiny group of merchants, no merchant would even begin to search the stuff, in a sea of information, unless they have to. Not to mention that most merchants wouldn’t be sure about what they need to search!

Processors, if they want to strengthen their relationship with their merchants must provide them with very easy to understand learning tools, such as short videos.

Communication

Processors need to be in constant contact with their merchants and give them updates and heads-ups when significant changes in fees or regulations are due.

Social media could be a handy tool for processors to inform their merchants.

I know that many sales agents work hard to keep their merchants well informed. They visit the businesses on a weekly or at least monthly basis and talk to them.

I have seen a lot more great individual sales agents with integrity and transparency, then processing companies.

Facilitate the technology

President Ronald Reagan famously said:

“Trust but Verify“

For the sake of argument, let’s assume that our merchants have total trust in their ISOs. How can we “verify” the claims of an ISO?

Based on everything I discussed so far, it’s evident that the merchants need a mechanism to inform them about the changes in the processing cost and explain the reason.

What merchants need a process through which they can understand the Statements of their account and be able to decipher it quickly, so the ISO can be held accountable for what promise and what they deliver.

Such a system will help ISO in two ways:

- To maintain and improve the excellent reputation of ISOs and build a better relationship with their merchants.

- As a sales tool to be able to analyze the Statement, and present an accurate comparison between what is and what could be the processing fees, and therefore, saving for a merchant.

As an ISO, you should be open to being scrutinized by your merchants. You cannot claim that you are honest, and your merchants trust you. There are always disgruntled merchants that could say otherwise about you.

Third parties, consumer advocate companies, help businesses, and merchants understand their rights and audit their Statements.

The majority of these companies perform manual and automated methods to come up with a better assessment of credit card Statements.

I, personally, know a Statment Analysis and Audit product by an entrepreneur from StatementSimple.Com.

Statement Simple has a robust Statement analysis features and some reports to compare and contrast past Statements.

I believe Jeffery King with his products has taken a critical step in helping both sides of the equation; merchants and processors.

By employing technologies such as OCR, Optical Character Recognition, and Machine Learning, these tools can magically and in seconds, audit and analyze most complex Statements, and inform the merchants of any changes, positive or negative.

The same technology is available to ISOs, and it allows them to quickly and accurately analyze merchant Statements in their efforts to gain new accounts.

Such tools will become necessary for any ISO to build a better relationship with their merchant and lower their attrition rate.

I reached out to Statement Simple, and they generously agreed to share more information about their product and technologies with me.

Before I share what I have learned with you, I have to let you know that I have no affiliation with Statement Simple or any of its subsidiaries. I am not employed, hired, or offered payment or favor in return for the introduction of Statement Simple in this article.

I also reached out to another company with a similar product, but they were not prepared to participate in this conversation.

Statement Simple

Jeffery King is a serial entrepreneur, he started this project over a year ago. His team has developed an outstanding product.

Knowing Jeff’s background in the payment industry, it comes as no surprise that his product has simplified the Statement audit to such a level that it can show you a Thumbs up, for no changes, and Thumbs down when there are changes that affect your rate adversely.

Merchants upload their Statements in PDF or image formats. In about 25 seconds, thousands of processes take place behind the scenes to figure out and classify the information from the Statement into an easy-to-understand report.

Keep in mind that Statements from different ISO have a different format and varied amount of data. A system that wants to work universally should be able to parse, audit, and report hundreds, if not thousands, of different Statements. It’s possible if we deploy concepts of AI and Machine Learning. That’s what you find in products such as Statement Simple.

The output is incredibly simple, and at a glance, a merchant can figure out what’s going on.

Statement Simple has a very complete API for developers and also several tools for ISOs to benefit from the Statement audit as a sales tool.

A white label version of the Statement Simple is also available.

Conclusion

Payment processing companies, have to raise the bar much higher when it’s about taking care of their merchants. A long and mutually fruitful relationship between merchants and their processors is always a boon for both of them.

What’s the average life of accounts in your company?